Don’t get trapped!

I’ve written a lot about credit cards and their many advantages. Things like earning rewards, extended warranties, travel benefits and fraud protection just to name a few. I wrote a post very recently about how credit cards are so much better than debit cards.

But credit cards can also be death to your finances. If you don’t pay on time and in full, you will be subject to late fees and interest. A LOT of interest. Credit card interest rates are easily in the double digits. And some cards can be in the 20% range. There is no reason anyone should be paying this much interest.

And consumers know this. Most adults know that not paying your credit card in full will lead to interest being charged to your balance. Knowledge isn’t the problem.

The problem is that the credit card companies have made it palatable for consumers to carry a balance and be charged interest along the way. The way they do this is by offering the “minimum payment.”

And it’s a complete scam that is designed to take money from consumers and turn it directly into profits for the credit card companies.

‘Til Debt Do Us Part

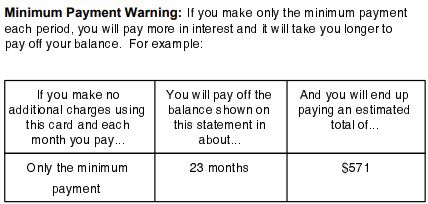

Here is a screenshot from one of my recent credit card bills:

Every credit card statement includes a message like this. They are literally telling us that making the minimum is bad for our finances and showing us how bad it is. In this case, the minimum payment was $25. That’s such a reasonable amount why wouldn’t I take the credit card company up on this offer?

Because the interest rate on this card happens to be 15%, and it would take me 2 years to get out of debt. And most people have multiple credit cards asking for a minimum payment. And all of this assumes that you will never spend another cent on your card (which is why it’s called revolving debt by the way. Debt is being paid off while new debt is being created).

So even with this warning from the credit card company itself, why do so many people just default to just paying the minimums on their cards? Because it’s just easier.

We live in a monthly payment type of society. And it just seems a lot cleaner to add your credit card minimum payment to your pile of monthly obligations. Put it on auto pay along with the car loan, student loan and mortgage. Just set it and forget it right? But in this case, forgetting about all of that interest building up in the background will destroy your finances.

Credit Card Debt is an Emergency

There is no such thing as a free meal. If you get a “free” meal, you will most likely be on the receiving end of a sales pitch. Just eat, smile, nod and be on your way.

Paying off credit card debt is the closest thing to a financial free meal you can get. Getting into credit card debt and paying 20% in interest month after month is not ideal. A situation like that, which many families find themselves in unfortunately, will keep you in financial prison forever.

But once you realize this and commit yourself to getting rid of that debt, no other financial decision matters. As high as credit card interest rates are, there is no investment out there that would justify you not getting rid of that debt as fast as possible.

If you’re paying 20% interest on a credit card, getting rid of that debt will be the equivalent of getting a 20% return on your money! While avoiding the debt is a much better first step, paying it off ASAP is the next best thing.

That’s why I consider credit card debt an absolute emergency! All discretionary spending such as new cars, vacations and fancy dinners out should be put on hold until the debt is gone. It’s much easier said than done but it’s the only way you’re going to get out of financial hell.

The worst part is that credit card companies don’t want you to feel this. They want you to feel comfortable shelling out 20% more money than you should each month. The goal is for credit card debt to become the “new normal”.

But you know better than that. Take care of credit card debt first and then focus on your other goals. That’s the closest thing to a financial free lunch you will get.

Enrich Yourself, not Visa

Banks make a TON of money off of credit cards. That’s why we will keep getting bombarded with credit card offers for as long as we live.

It’s actually pretty absurd. Banks are simply offering a 30 day loan and charging an exorbitant amount of interest for it. At least with an auto loan you can enjoy your car and get some use out of it. But with credit card debt there is no collateral that you can really make use of. Those fancy dinners out are just a memory at that point.

So don’t fall for the minimum payment scam. There is no use for it except to keep consumers in debt for their entire life. It’s all very sinister if you really think about it. People become depressed and even commit suicide because of debt. But as long as banks continue to profit off of credit cards, they couldn’t care less.

Free yourself and pay off your debt in full!

Thanks for putting this into perspective! Can I put my CC on auto-pay every month for the current total balance or is it always for just the minimum payment?

All the credit cards I’ve dealt with give you the option of auto pay for the minimum payment AND the full balance of the statement. So as long as you choose the full balance you should be good. But I’m sure the credit card companies would like you to automate the minimum payment and just forget about it!

Also, do you have an opinion and /or know any advantages of setting CC payment due dates at the end of the month(31st) or the beginning of each month? Which would you choose personally? I want to change my monthly payment due date on my CC to align with my other cards and my student loan payments. These are all currently set to the 1st of each month.

I don’t really have an opinion on this. I do know that most cards will allow you to change the date. You could change it so your due date lines up with your pay day in order to make things more efficient. But I don’t see much reason to worry too much about that.