Your credit score is one of the most overlooked parts of personal finance. Most people don’t know what their credit score is, why it’s important, what contributes to your score and how you can improve it. I will go into all of that and more. If you take away only one thing from this discussion, it should be that improving your credit score is a sure fire way for you to save THOUSANDS of dollars across a lifetime. This is because if you have a great credit score, you will get the best interest rates on mortgage and car loans. Getting the best rate can save you tens of thousands of dollars on your mortgage alone.

Credit Score basics

Your credit score is a number between 300-850 that lenders use to determine if you are a risky borrower or not. Generally speaking, the lower your credit score, the more risky you look to lenders. Which means they will offer you the higher end of their interest rates. The opposite holds true for those with high credit scores. This means you will get a great rate for your mortgage, car loan and be accepted for all of the awesome credit cards available.

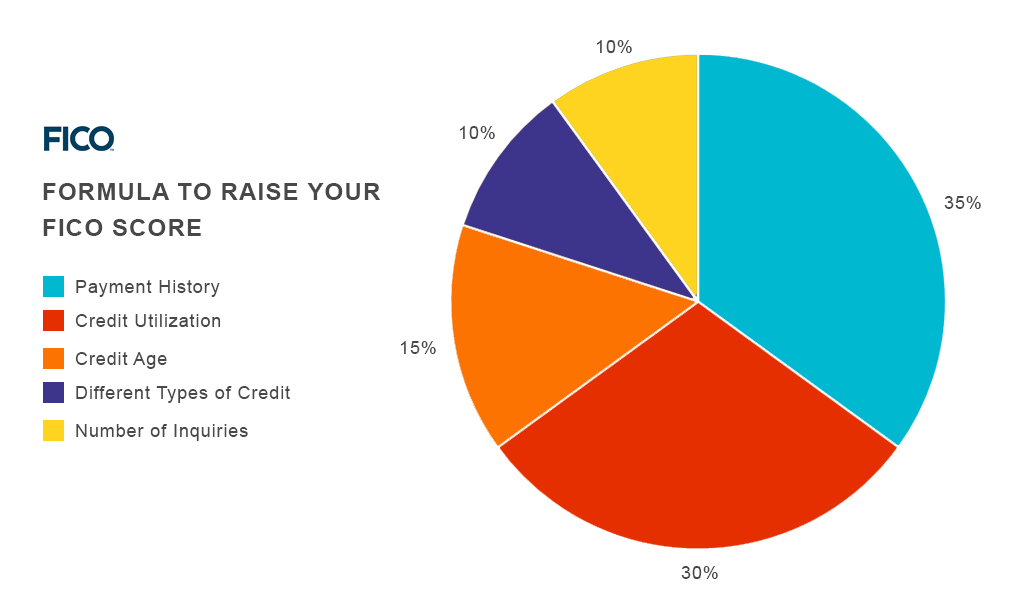

What goes into your credit score? Let’s go straight to the source: The Fair Isaac Corporation (FICO). Your credit score is also called your FICO score, so it pays to listen to what they tell you. Here is a nice little pie chart that lays it all out there for you:

Creditsesame

Looking at the chart, it’s easy to see what makes up the majority of your score: payment history, amounts owed and length of credit history. So as long as you make your payments on time, don’t go near your credit limit on your cards and do that for a few years, your credit score will most likely be excellent.

Conversely, there are a few things that can absolutely KILL your credit score. And it’s a lot easier and faster to lower your score than it is to increase it. Making late payments is the #1 surefire way to kill your credit score. Looking at the chart makes that obvious, but it also makes perfect sense from a lender’s point of view.

If you’re shopping for a home loan, the lenders will look at your credit score. If your score is low, it tells them you probably don’t pay your bills on time. While this may or may not be a fair judgement based on one number, a low credit score will nonetheless discourage them from offering you their lowest interest rates.

And late or missed payments can include anything: Credit card bills, past mortgage payments, rent, car payments, cell phone bills, utility bills and student loan payments. All of this stuff gets reported to the credit bureaus, so staying on top of your payments is vitally important.

Do Business Online

What’s the best way to make all of your payments on time? Do everything online. This makes things really easy as you can just bookmark all of your monthly bills and pay them right online. Many also allow automatic payments, which pretty much guarantees on time payments. Use technology to your advantage when it comes to your credit score. Your future self will thank you.

Another way to hurt your credit score? Getting really close to your credit limit. This usually refers to credit cards, and it specifically refers to your credit utilization ratio.

If you have a $20,000 credit limit across all of your cards, and are consistently charging $19,999 every statement period, this shows lenders that you’re using too much credit. You are a risky borrower in their eyes. There are two ways to fix this. The obvious one is don’t spend up to your credit limit! Either switch to cash for some payments or go through your spending history and cut out the unnecessary stuff.

Another way is to request a credit limit increase. Just call the number on the back of your credit cards and ask if you can get your limit increased. Some will do it and some won’t. But any increase in your credit availability will help your ratio. Increasing your credit limits and decreasing your spending at the same time would be the ideal way to go.

Conclusion

According to the FICO pie chart, new credit and types of credit used also contribute to your score. This is only 20% of your score, so it’s not really worth focusing a lot of your time on, especially if you have problems with late payments. Opening a lot of lines of credit will temporarily decrease your score a few points, but it will go back up once they realize you’re still making your payments on time. Focusing on late payments and high credit utilization ratios, the two credit score killers, is the quickest and most important way to improve your score.

There are so many of those free trial credit monitoring services, there’s no reason not to know your FICO score. As long as you remember to cancel before they charge you!

Great point Stefanie. Thanks for the words of wisdom!

Conversely, there are a few things that can absolutely KILL your credit score. And it’s a lot easier and faster to lower your score than it is to increase it. Making late payments is the #1 surefire way to kill your credit score.

I always try to pay my CC balance every cycle. And I usually only have 3-4 credit cards allocated to certain types of expenses. I feel like this makes you more disciplined to use credit for your intended purposes and lower the risk of over-use. So many times I will just rip a piece of mail that has a credit card offer without even opening the envelope since all of these can also be found and completed online. 🙂

Exactly most people would do well to just remember to pay off their credit card balance every month. Too many people get caught doing balance transfers or trying to get sign up bonuses only to end up with more debt.

I always encourage people to pay their credit card twice each month to avoid ever forgetting to make a payment. It’s worked well for me the past few years. You can automatically have things pay as well, but I think there is some value of actually logging in and seeing what charges are hitting your accounts.

I never considered the twice a month tactic. I’ll have to try that. I also like logging in and viewing my statements just to make sure nothing fishy is going on.

Yes I make wkly payments for years on my cards But still get fined i send

every friday 52 wks a year and pay 12 fines a year I get paid wkly so i pay wkly why can’t i get any help from them on this do they have wkly plans i get wkly not mothly they don’t under stand that