Get some quotes people

This post contains affiliate links

People tend to need some hand holding when trying something new. I’ve found this to be the case when recommending student loan refinance to colleagues.

I recently wrote why everyone with student loans should consider refinancing. The best that could happen is that your interest rate goes down substantially and you save tens of thousands of dollars over the life of the loan. The worst that could happen is that refinancing is not beneficial and you stay right where you are.

Nothing to lose at all.

And while people generally like doing things that will benefit them, sometimes a little prodding is still necessary.

For example, I know it’s a good idea to try and fix things around the house myself before I call someone. But I need to watch a couple of good step by step videos on Youtube before anything actually gets done. That’s just the way I am.

Many people are like this when it comes to saving money. They know it’s a good idea to open up a savings account and contribute to it automatically, find a less onerous checking account or sign up for a rewards credit card. But sometimes a little kick in the pants is needed to get going.

This post will serve as that kick in the pants. I will show you how easy the student loan refinance process is and what companies you should consider. Let’s get started.

(I will use screenshots from SoFi since they do not require a hard credit check before getting quotes. More on that later.)

Step 1: Go to the lender’s website

Just type in SoFi.com (or better yet use this link and get $100 if your loan gets approved.)

Most online student loan refinancing companies have easy to use interfaces. Once you’re on the home page, simply click “Find My Rate” on the top right.

Step 2: Enter Your Personal Information

In order to give you an accurate quote, lenders need some information from you. The type of information required will vary between lenders, and some lenders will do a credit check before you get your quotes. So the experience with each company will vary.

(By the way I did not hack into Bill Nye’s SoFi account I just made up an account with his name. I’m fairly sure he doesn’t have a need for student loan refinancing.)

Typically, the information most lenders require is:

-Basic demographic information

-School information

-Employment information

-Current student loan balances and rates

-A little later in the process, you will probably have to send proof of income and a picture of your license or passport.

Some people are wary of giving companies too much information. This is not really anything to worry about. In reality, Facebook has a whole lot more information on us than these companies ever will, so I’m okay with letting them know how much money I make.

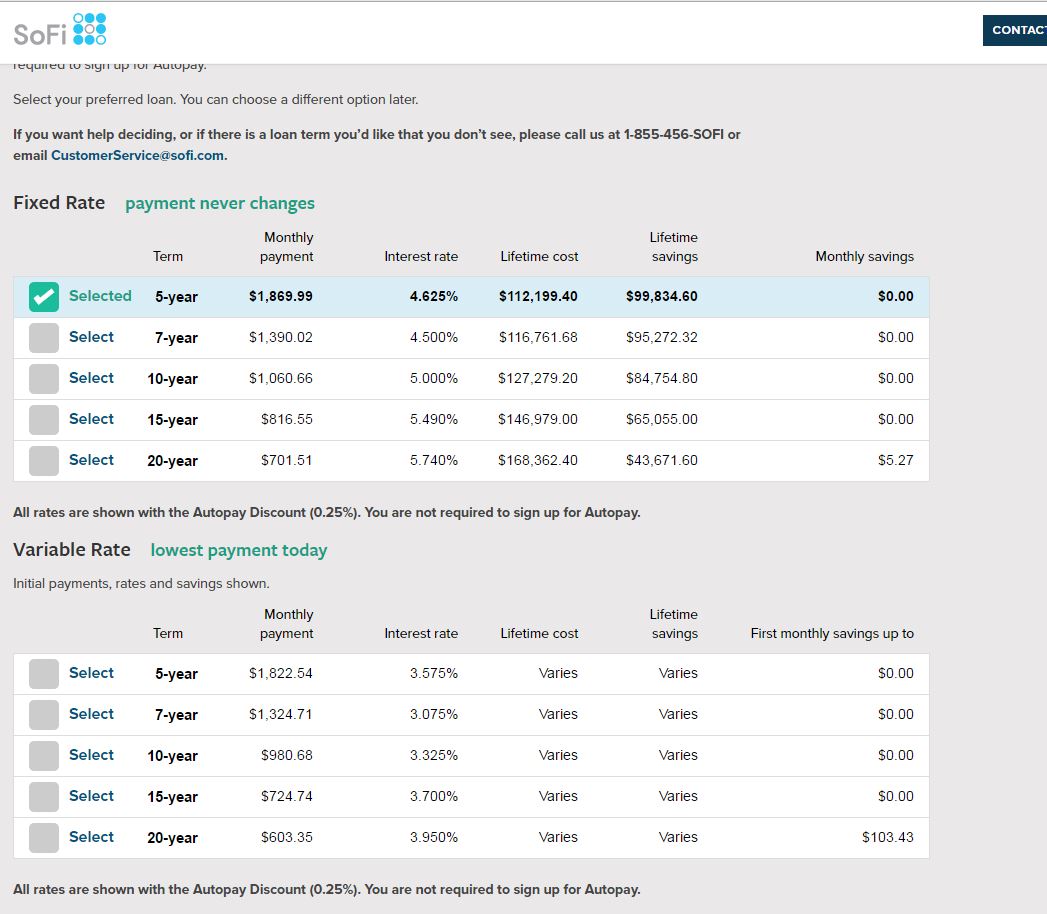

Step 3: Analyze your quotes and make a decision

This is where the fun begins. After you enter all of your information, companies will run a soft or hard credit check. A soft check won’t affect your credit score but will still allow you to see some quotes which are going to be pretty close to your actual quote. A hard credit check will show up on your credit report but will give you very precise quotes.

With the example I used, I assumed a student loan balance of $100,000 with a 7% interest rate and a 25 year term. The minimum payment would be $706.78. Making just the minimum payment over those 25 years would amount to a total payment amount of $212,000. More than double the original loan amount!

I advise to go with the shortest payoff period you’re comfortable with and can afford. But as you can see, even if you go with a 20 year term it would still result in a lifetime savings of more than $43,000 with a slightly lower than original monthly payment! That’s why I say refinancing is a no-brainer.

A shorter payoff term will also result in a lower interest rate. So the shorter you can go, the better it will be.

Fixed or Variable?

The other consideration is if you should go with a fixed interest rate or a variable interest rate. This discussion deserves a post of its own (that’s a good idea!), but if you opt to go with a longer payoff period, about 10 years or longer, I would suggest sticking with a fixed interest rate.

Interest rates are sort of predictable as far as if they will be going up or down, but the uncertainty lies in when that will happen. Right now in 2016, for instance, interest rates are pretty low so they are bound to go up at some point.

But that could be 6 months from now or 6 years from now. There is too much uncertainty over a long period of time. So for shorter term loans, less than 10 years, variable rates are a good bet and for longer term loans, it’s better to stay with fixed. Everyone has different risk tolerances so use that as a general guideline.

The last thing to consider is that your rates will probably vary from my results, and will probably vary from someone in your same class. Companies take into account your credit score, credit history, loan balance, interest rate, where you live, where you work and who knows what else. The screenshot above is just for illustrative purposes, so make sure to get quotes after putting in your own personal information.

So Which Refinance Company Should I Use?

The student loan refinance arena is growing rapidly. I keep get letters in the mail from new companies claiming they can refinance my loans at the lowest rate possible.

But let me give you the short answer. There are only two companies worth your trouble:

#1: Earnest (get a $200 bonus by using this link)

#2: SoFi (get a $100 bonus by using this link)

I ended up going with Earnest for my refinance, just because their quoted rate was .05% lower than SoFi’s. Everything else was pretty much the same with both companies.

Both companies make the onboarding process easy and both companies have great customer service. You may get different quotes because both companies have different underwriting standards, so get quotes from them both and compare.

If you really truly want more quotes, a good place to look would be Magnify Money. They will give you a list of all the best student loan refinance companies. They are also a great resource to find the best checking and savings accounts.

Looking at the potential savings from refinancing I don’t know why anyone would not get a few quotes and see how much they could save. Refinancing is not a good choice for everyone, but getting quotes online is so easy it really is in your best interest to just take a look.

So to conclude: Earnest. SoFi. See how much you can save.

I’ve been meaning to go through SoFi for some time now just to see what sort of rates and options we would get. I’m all about lower interest rates so if it’s a good deal I will consider it.

Yeah definitely no harm in checking. And for people that have good credit scores the rates can be really good.

I went ahead and checked this a few months back (mainly to go through the process for a blog post on it) and because I’m so far along in my loans I would literally save only ~$100 by refinancing. Not nearly enough to get me to go through with it!

Yeah for some people refinancing isn’t worth it. But there is no harm in checking since most sites just do a soft credit pull

This is great information! I’ve always thought about refinancing my student loans but never actually looked into it because I got too comfortable with my current IBR plan. Definitely time to start looking at these other options.

Yeah definitely worth a look. Seeing how much you pay over the life of the loan is important as well. While the IBR payments may be lower, you could be paying a lot more in interest over time. If you can afford to get the loans paid off quicker, that’s a smart way to go!

The only consideration is for those with Federal student loans. They could potentially be giving up their access to programs like IBR or public loan forgiveness if they refinance. Always good to check and get a quote though.

Right new grads should check to see if any of these programs would be a good fit for them. I’m not a HUGE fan of IBR because it doesn’t change your loan balance but just decreases your monthly payment amount, but I could see how some people might need it. But for anyone making decent money, refinancing could be a better option. Thanks for the comment!

I have a six figure income and excellent credit, yet my student loans are well into the six figures as well. I’m currently on REPAYE plan because that’s all I can afford at the moment with two kids in daycare. I am counting on the forgiveness after 25 years, even though I know that may be taxable. Would you say it’s a good idea for me to refinance? I don’t want to give up the forgiveness option unless there’s a significantly lower interest rate possible

Government programs are definitely worth participating in if that’s the only way to swing the monthly payments. I would say check out the rates and see how much you could save over the life of the loan. There’s no commitment to look at some quotes. The interest rate is a factor but the bigger factor is how much you would pay pay the life of the loan. Even at a lower payment, 25 years is a long time. You might come out ahead over the life of the loan with a refinance. I don’t know your exact situation, but personally I was able to make a big dent in my loans by cutting a few things around the house and plowing that savings into my loan payment. Feel free to email me if you have any more questions. Best of luck.

Earnest was definitely my choice when I refinanced! Heard good things about SoFi but didn’t pan out in my favor.

I’ve used both for my wife’s loans and my loans. Their underwriting process is different so you don’t really know where you’ll get the best refinance rate until you try. My advice to colleagues is to get rates from 3 different companies and see which comes out on top.

An interesting thing I noticed on this post. This was post was published on July 2017 but there are comments from 2016??!

Ha yes seems weird but the post originally ran in 2016 but I just updated it in 2017.

Hi! I’ve heard from various colleagues who have refinanced with similar backgrounds, credit scores, and loan amount, however the interest rate is much different. One stated it was because of the time of year that they refinanced. Are you aware of a certain “time” thats most ideal for refiancing? Can you explain why you prefer refinance over the IBR plans? Also would you advise tackling your debt first prior to doing any investment? Thanks!

Hi there. I’m not sure about a specific time to apply but every company has different underwriting methods. The biggest factors though are your credit history and income. Also, you usually get better rates if you’re employed rather than self employed. Those things will be the biggest things that will determine what kind of rate you will get.

Refinancing is great for many people, but going with the government programs will be a good idea for some. Especially for those with very high loan balances since you can get them forgiven for the most part in 10 years if you qualify. If money is tight you can also reduce your monthly payment or request a forbearance, which you can’t really do after refinancing.

As far as paying off debt or investing, that is a big question which books have been written on. It depends on a lot of things such as your personality and the interest rates of the loans. But my short answer would be to take a hybrid approach. Make a plan to be debt free in a reasonable amount of time and pay that much. Then use the rest for investing. Especially if you’re young and right out of school, compound investment growth is something that is very powerful