(Hey everyone. The following is a guest post from my friend Ryan, who specializes in financial planning for physicians. He’s doing great work since many physicians and other health professionals are clueless when it comes to their finances. In this post Ryan talks about a unique aspect of doctor’s credit scores. Enjoy!)

![]()

As a financial planner who specializes in working with doctors and their families, I’ve realized over time that many doctors do have high credit scores. Having a high credit score enables doctors to get competitive interest rates on mortgages, car loans, and more. It also shows lenders that they’re not only accomplished physicians but responsible borrowers who pay their bills on time.

I’ll expand more why doctors typically have high credit scores by outlining how a credit score is actually calculated. That way, if you’re a doctor who wants to raise your credit score in anticipation of a big purchase, you’ll know the steps to take to increase your score to get the best opportunities available to you.

Here are some of the reasons why physicians typically have high credit scores:

1. Length of Credit History

The length of your credit history definitely factors into your score. For many doctors, taking out student loans is the first step in establishing a credit history. If you start taking out loans as an undergraduate, you’ll have at least 7-8 years of credit history by the time you finish residency.

If you didn’t take out student loans as an undergraduate but you did as a graduate student or medical school student, you’ll still have a few years of credit history under your belt. This helps to improve your score.

2. Payment History

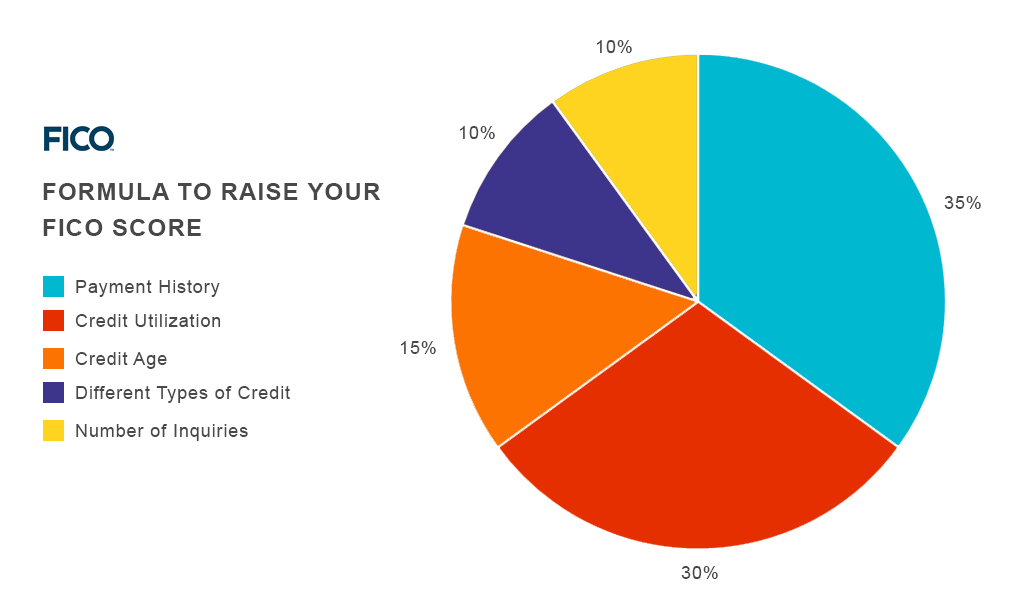

Your payment history is probably the most important aspect of your credit score because it makes up a whopping 35% of your score. This is the part of your score that shows lenders you’re a worthy investment and that you’ll pay them back on time.

The great news is that once you take out student loans, you’ve started a credit file. Even if your student loans aren’t due yet, your account is in good standing month after month while you’re in school. Lenders love to see this.

If you have credit cards in addition to your student loans, be sure to pay these on time as well. Even if your student loan accounts are in good standing, missing a credit card payment will be detrimental to your score. So, make those payments on time every time solely because your payment history factors so heavily into your overall credit score.

3. Debt Utilization

Having a low debt utilization percentage is a fancy way of saying that you’re living within your means. Your debt utilization percentage is how much debt you have relative to the amount of credit available to you. So, if you have 5 maxed out credit cards, your debt utilization percentage will definitely hurt your credit score. However, the more available “space” you have on your revolving credit, like credit cards, the better your credit score will be.

The great news is that student loans are considered installment debt, not revolving debt. They’re a different type of debt than credit cards and thus aren’t factored into this debt utilization score. So, if you have hundreds of thousands of dollars in student loans but you’re not carrying a balance on your credit cards, your debt utilization percentage will be low, which is good for your credit score.

—

Now that I’ve listed the three parts of a credit score where doctors typically excel, I want to take the time to write about what can hurt your credit score too.

After all, the goal in life is generally to become financially well off, self-sufficient, and happy. Having a strong credit score can enable you to get lower interest rates on some of your biggest purchases, saving your thousands and thousands of dollars over the course of your life. This, in turn, will allow you to use your hard earned money for the things you actually want to do.

So, be aware of these two parts of a credit score as well:

1. Credit Mix

Lenders actually want you have a few different types of loans, called a credit mix, because it shows them that you’re able to successfully handle various types of payments like a house payment, credit card payment, and a car payment.

If you only have student loans, this could lower your score, but if you mixed it up a bit (see what I did there?) you could raise your credit score by a few points.

For older doctors who own houses, cars, and have business loans, it’s easy to have a decent credit mix. However, newer doctors who are just finished training might not have many different types of loans.

Keep in mind that credit mix is a small portion of your score and you shouldn’t go and take out loans that you don’t need for the sole purpose of improving this part of your score. However, if you need to bump up your score a few points to qualify for a better mortgage interest rate, diversifying the types of loans you have is something you can try.

2. New Accounts

This might seem a little counter-intuitive to the point mentioned previously, but it’s something worth mentioning. Basically, lenders don’t like it when you open a bunch of new accounts at once. It signals to them that you’re in need of a lot of credit quickly or that you’re somehow in need of financial help.

So, avoid opening several different credit cards in one year. At the same time, avoid closing your old accounts. Lenders might not like to see a lot of new accounts but they love seeing old accounts in good standing. It shows that for many years you’ve been good about having loans and paying them back on time.

—

Keep in mind that as you go through your daily life, your credit score will fluctuate. It’ll fluctuate as you pay down debt. It’ll change if you refinance your student loans. It will also change if you get a new travel credit card or a new house. It’s okay for your score to go up and down some, as long as you’re consistently making your payments and checking your credit report regularly to ensure your identity is safe. I tell my clients to sign up for an account at Credit Karma because it’s free, you can check your score whenever you want, and you can dispute anything that’s not right your credit report easily and most importantly, quickly. After all, you don’t have a lot of free time to worry about your finances, right?

So, the good news for all the doctors reading this is that you probably have a high credit score already due to the points I mentioned above. However, if you don’t or if you’re looking to boost your score a few points, that’s absolutely possible by understanding how your credit score is calculated and knowing how you can improve it over time.

Ryan Inman is a fee-only financial planner who specializes in helping physicians and their families build a solid financial future through his firm, Physician Wealth Services. As the husband of a physician, Ryan has a unique insight into what it’s like to be a part of a physician family and thoroughly enjoys helping his clients. To schedule a free 30 minute consultation, feel free to contact Ryan at any time.

Good overview, Ryan. I like that you are focused on just one niche and the unique needs of that demographic. I’d be curious to hear how many doctors are interested in getting out of practice within a short period of time, i.e. 5-10 years. Seems like it’s a labor of love after a while. I know my pulmonologist who I saw from age ~3 to 21 could have retired years ago but just loves the kids he works with and how he can impact their lives.

We absolutely love your blog and find the majority of your post’s to

be what precisely I’m looking for. Do you offer guest writers to write content in your case?

I wouldn’t mind composing a post or elaborating on a number of the subjects you write in relation to here.

Again, awesome weblog!

Financial difficulties point to appear unexpectedly. Problems can be different, and there is always one solution – an online loan https://getfastcashus.com/1-hour-payday-loans-online-no-credit-check.php. It is this company that will help get rid of real difficulties fast and effortlessly. It does not require collecting documents, visiting a credit institution, and confirming your solvency. You can apply online anytime. We provide 24*7 solutions on Getfastcashus.