Most major religions have the concept of sin. From my understanding of my own religion and other major world religions, sins are detestable actions that take you further away from the Divine. Some sins have the double whammy effect of harming your soul and potentially messing up your life on Earth too. Infidelity or drug use, for example.

Even those who don’t subscribe to a particular religion believe there are some acts that just should not be done. Murder, theft and oppression come to mind.

I would love to go more into this, but I’ll save that for the theology blog.

I wanted to discuss some financial “sins” that can take you away from the “divine” (financial freedom) and can destroy your life. While some financial sins can potentially affect your afterlife (think embezzlement and money laundering), the sins discussed here will be more of the mortal world variety.

Committing these sins can derail your finances and can sometimes be a gateway to even more financially devastating actions. In no particular order, here are some of the more blasphemous things you can do to your finances:

Raiding tax deferred retirement accounts early

Retirement accounts such as 401(k)’s and IRA’s are the backbone of a solid retirement plan. You contribute into these accounts during your younger working years so that you can hopefully enjoy a stable retirement down the road.

The government has put some restrictions on these accounts so people won’t just withdraw money from them as they please. A common retirement account is the Traditional IRA. According to the IRS (no relation to IRA), if you withdraw funds from a Traditional IRA before age 59.5 you will have to include the withdrawal amount in your taxable income along with paying a 10% penalty.

That’s a hefty fine for putting your hand in the retirement cookie jar. If you are in the 22% federal tax bracket and you withdraw $100,000 from your IRA, you lose $22,000 of it from taxes. Add the 10% penalty and your $100,000 withdrawal becomes $68,000!!

Think of withdrawing early from your retirement account as robbing an old man version of yourself. That seems cruel. You’re also sort of robbing your current self too with the huge tax hit.

So unless you’re in dire straits, don’t consider withdrawing from retirement accounts. Your older self will thank you.

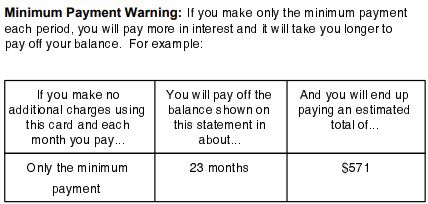

Carrying credit card debt

There used to be a time when credit cards didn’t exist. People used to pay for things with cash and for the most part didn’t get into monstrous debt.

Nowadays, credit is easy to get which makes it much easier to get into debt. Funny how that works.

In 2017, the average household credit card debt was a little over $6,000. That is a bad enough number, but there are a lot of households that have no credit card debt. So the ones that do have debt probably have much more debt than $6,000.

The sinful nature of credit card debt has to do with their super high interest rates. Rates can vary widely, about 7% on the low end and 25% on the high end. These types of rates will make it almost impossible to make any money investing. Those high credit card interest rates will wipe out any potential investment gains.

Thankfully there are a lot of options to help you jump start your debt repayment. You can do a balance transfer to a card that has a 0% promotional rate. Just make sure to pay it all off before the promo rate ends.

Many companies, such as Lightstream and SoFi, also offer personal loans with much lower rates than a credit card would offer. You can use these funds to pay off the credit card debt and work on paying back the much lower interest loan.

Buying a home when you can’t afford it

The American Dream of owning a home is alive and swell. For whatever reason, people don’t think they’ve “made it” unless they own a home. Which is dangerous because there are lots of people who should be renting instead of owning due to the current state of their finances.

Owning your own home can be downright expensive, especially if you stretched your home buying budget a little too much. Not only do you have the monthly principal mortgage payment, you also have interest to pay to the bank (rates are rising!), property taxes to pay to the state and homeowners insurance to the insurance company.

Then you need to factor in maintenance costs. Even if you buy a brand new home, things will break down and light bulbs will need to be changed. And everything has a shelf life and will eventually need repair or replacement. That includes the dishwasher, water heater, air conditioner and everything else that keeps your home comfortable.

If all of these potential costs make your head spin, maybe you should reconsider buying a home. Paying rent is a simple monthly expense with no maintenance costs or strings attached.

The sinful part of buying a home you can’t afford is that it handicaps any other financial or personal goals you may have. It gets much harder to find money to invest or travel if everything is tied up in the house.

These are three big financial sins that should be avoided by all. One thing I’ve learned in life is if you can avoid the big sins and make small consistent virtuous decisions along the way, you will be just fine.